By Steve Tabrizi, Chief Operating Officer – Broker/Owner REMAX Hallmark

The story being marketed is simple and wrong. Real “saved” REMAX® from its debt. Compass “rescued” Anywhere from declining margins. eXp “absorbed” NextHome’s franchisees who couldn’t make it alone. It’s a tidy narrative, and it’s nonsense.

Strip away the press releases and the social media pretender experts or as we politely call them, influencers and a different picture emerges. In each of these deals, the buyer is acquiring the exact thing it spent the last decade telling the industry was obsolete. Real, with no franchise income and no broker-operator layer, bought 50 years of both. Compass, after a decade of calling itself a technology company, bought six legacy franchise brands. eXp, after a decade of arguing the cloud model made offices irrelevant, bought 500 franchisees and changed its ticker to AGNT. These aren’t rescues. They’re confessions paid for in cash, stock, and a billion dollars of new debt.

Nobody got saved here. Two halves of a broken industry just realized they couldn’t survive without borrowing each other’s missing pieces.

Look at what each side is actually buying. Real has $2 billion in revenue that flows through its books as agent commission pass-through. Strip that pass-through away and the company keeps about nine cents on every dollar. Last quarter it lost money on a GAAP basis. It has no international footprint of any consequence. And critically, it has no recurring broker-operator layer income, its entire revenue stream depends heavily on the same economic cycles that just punished the rest of us.

REMAX®, on the other hand, is a 50-year-old global brand. 149,000 agents across 110 countries. Master franchise structures throwing off recurring fees. Independently owned offices with broker-owners who actually train, recruit, and develop talent at the local level for actual profit, not for rev share, actually building a saleable business. That isn’t a company being rescued. That’s a company being acquired for the assets the buyer never bothered to build or tried to build through rev share but wasn’t willing to take the 50-year journey to do it.

Compass spent ten years calling itself a technology brokerage that also respected that brick-and-mortar matters. The verdict from public markets was less generous, it traded for years like a real estate brokerage with an expensive software bill. So, Compass bought Anywhere, the parent company of Coldwell Banker, Century 21, Sotheby’s, Better Homes and Gardens, and ERA. Six legacy brands. Tens of thousands of independently owned franchisees. The exact infrastructure Compass’s original pitch said was obsolete.

eXp bought NextHome for the franchisees. And then changed its ticker to AGNT. After a decade of telling the industry that cloud beats office, that revenue share beats franchise, and that local operators were a tax on agent production, eXp paid real money to buy 500-plus franchisees and renamed itself after the very thing it spent ten years saying was optional. The ticker change is the confession the press release wouldn’t write.

Yes, REMAX® is carrying $436 million in debt. Yes, anywhere has been managing its own leverage. Yes, balance sheets matter. But framing these deals primarily as debt-relief operations reveals more about the writer’s lack of financial education than it does about the deal.

REMAX® wasn’t bought because it had debt. REMAX® had debt because it had been a real, cash-generating business for long enough to lever itself in the first place. You don’t get to $436 million of term debt by being a fragile company. You get there by having decades of recurring, predictable income that lenders are comfortable underwriting against. That’s not weakness. That’s the exact profile that supports borrowing, the opposite of a cloud brokerage that survives on equity issuance because there’s nothing for a bank to lend against. Banks don’t lend against agents. Agents are moving targets with no long-term contracts to predict income from.

Meanwhile, Real is taking on $550 million of new debt to do this deal. The combined company will spend the next two to three years deleveraging, paying down loans rather than rewarding shareholders. If “debt” is the bad guy in this story, the supposed rescuer just signed up for more of it than the company it was rescuing.

The buyer is taking on more debt than the seller had. That is not a rescue. That is a leveraged acquisition with a marketing department.

Before we get into the math, one quick definition. GAAP stands for Generally Accepted Accounting Principles, the standardized rulebook every public company has to follow when reporting financial results. “Adjusted EBITDA” is the number companies tell investors at the Instagram party. GAAP is the one they have to tell the government. Same quarter, Real reports +$14.9M in Adjusted EBITDA and a $3.4M loss on a GAAP basis. Both are technically correct. Only one of them is the truth. Keep that in mind for what follows.

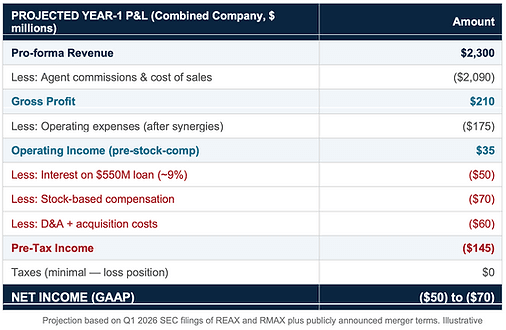

Let me walk you through what happens to a dollar after this deal closes. No spreadsheet voodoo. No CFO talk. Just one dollar, and where it actually ends up.

A client signs at the kitchen table. The cheque is written. A dollar of commission heads into Real’s books, where it gets booked as “revenue” and quoted proudly on the next earnings call.

Then it leaves again. Roughly 91 cents of that dollar walks straight back out the door to the agent who actually did the work. Welcome to brokerage, where the company is essentially the FedEx of money, it picks the cheque up, drives it across the table, hands it to the agent, and gets to count the whole trip as “revenue.” Impressive on the income statement. Less impressive when you remember they never owned the package.

So, we’re down to 9 cents. That’s gross profit. That’s the entire bag of chips the company gets to live on.

Out of those 9 cents, the company has to feed everyone who isn’t an agent. The CFO. The marketing department. The technology bills. The lawyers (so many lawyers). After all that, we’re down to maybe 3 cents. But wait. We’re not done.

Real just borrowed $550 million to buy REMAX®. Banks, surprisingly, do not lend $550 million out of friendship. Interest on that loan runs roughly $50 million a year, about 2 cents off every dollar of revenue. Goodbye, 2 cents. The bank thanks you for your service.

Then there’s stock-based compensation, the magical accounting trick where companies pay executives in stock instead of cash and then politely ask everyone to pretend it isn’t a real expense. GAAP says it is. So another 3 cents per dollar quietly vanishes into the executive comp pile.

Then add depreciation, integration costs, more lawyers (told you), and a few “one-time” charges that somehow show up every quarter. Call it another 3 cents.

Add it all up. The actual projection, in plain English, looks like this:

Every dollar that walks into Real’s books walks back out as a 2 to 3 cent loss. The agent got 91 cents. The bank got 2. The execs got 3 in stock. The lawyers got two yachts. The company got an IOU.

The path back to actual profit is real but slow. Year 1: bleed. Year 2: roughly breakeven once $30 million of “synergies” (corporate-speak for layoffs) kick in. Year 3: possibly $60 to $90 million of actual net income, if interest rates cooperate, if agents stay, if the housing market doesn’t sneeze. Three years from now this might look brilliant. Or it might look like the most expensive way ever invented to discover that brokerage is a thin-margin people business that doesn’t transform into a software company just because you wish hard enough.

None of this happened by accident. Leadership on both sides spent ten years getting the basics wrong. Cloud leadership built their pitch on agent count and revenue share. They never gave enough weight to the one thing that actually keeps a brokerage healthy long-term: agent productivity. The producing agent, the one closing fifteen or twenty deals a year and bringing real value to clients and to the company, was treated as a number on a leaderboard instead of a person worth developing. The model rewarded recruiting, not producing. When the market slowed in 2024, the math fell apart, because you cannot run a company on agents closing three deals a year, no matter how many of them you have.

Legacy brand leadership made the opposite mistake. They sat on a strong brand and assumed that was enough. It wasn’t. While the cloud players were busy building the wrong technology, the legacy brands were not building any. They failed to give their operators and their producing agents the tools that would actually make their work easier, the kind of platform that helps a broker-owner run their office, helps a team leader manage leads, and frees up an agent to spend more time selling and less time on paperwork. The brand kept them alive. The lack of technology is what made them targets.

One side built the wrong tech for the wrong customer. The other side competed in building the same wrong tech. Both sides were certain they were right. These deals are the bill for that certainty.

So back to Real and REMAX®. Compass and Anywhere. eXp and NextHome. Strip away the rescue narrative and what’s left?

- Three companies admitting they can’t scale to true profitability on a single model.

- Three companies acknowledging that brand, franchise structure, and local broker-operators are not optional, they are part of the operating system.

- Three companies, combined, taking on over a billion dollars of new debt to buy the parts of the industry their original thesis dismissed.

None of this is a rescue. All of it is a confession. The industry doesn’t need a winner of the cloud-versus-franchise debate. That debate is over. What it needs is leadership willing to say out loud what these transactions are saying with their cheque books.

Agents are the engine. Broker/Owners/Mentors/Team Leaders are the multiplier. Technology is the leverage. Brand is the trust. You need all four. You always did.

For the agent reading this, the takeaway is simple. You are not being rescued. You are not being disrupted. You are being recognized, slowly, expensively, and a decade too late, as the actual asset the entire industry is built on. The companies acquiring each other right now are paying real money to admit what should have been obvious from the start. Pick the brokerage, business operator or team leader that already knew it and is focused on building your business.

By Steve Tabrizi, Chief Operating Officer – Broker/Owner REMAX Hallmark